The transition to solar energy represents one of the most impactful decisions homeowners and businesses can make in 2026, but the upfront solar panel cost often creates a significant barrier. The good news? Solar financing has evolved dramatically, making renewable energy accessible to everyone—regardless of available capital. Whether you’re a homeowner in Gujarat looking to reduce electricity bills or an industrial facility seeking to lower operational costs, understanding your financing options is the first step toward energy independence.

At Heaven Green Energy Limited, we’ve helped thousands of customers across Gujarat navigate the complex landscape of solar financing since 2017. This comprehensive FAQ guide addresses every question you might have about funding your solar installation, from traditional loans to innovative zero-down payment schemes, government subsidies, and everything in between.

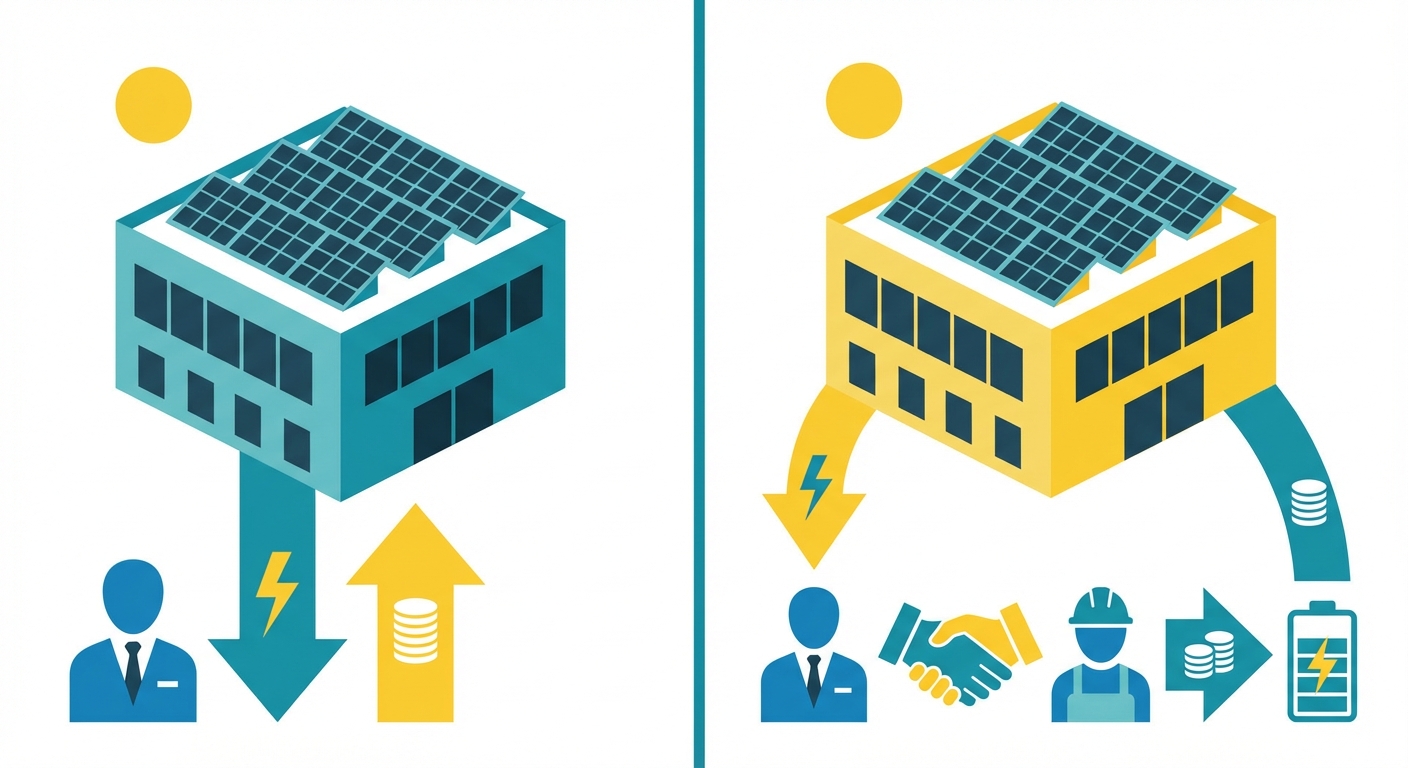

Understanding Solar Financing: Making Solar Energy Accessible to Everyone

Solar financing refers to the various payment methods and funding mechanisms that allow property owners to install solar energy systems without paying the full cost upfront. In India’s rapidly growing renewable energy market, solar financing has become the bridge between aspiration and implementation, enabling both residential and commercial customers to adopt clean energy immediately while spreading costs over time.

The solar industry in Gujarat has witnessed remarkable growth, with the state leading India’s renewable energy transition. However, the initial investment for a quality rooftop solar Gujarat installation can range from ₹60,000 to ₹1,00,000 per kilowatt for residential systems, and significantly more for commercial and industrial solar Gujarat projects. This is where financing becomes crucial.

Modern solar financing options offer flexibility that wasn’t available even five years ago. Today’s solutions include:

- Solar loans with competitive interest rates that allow you to own your system from day one

- Lease agreements where you pay a fixed monthly amount to use the solar system

- Power Purchase Agreements (PPAs) where you only pay for the electricity generated

- Zero-down payment schemes that eliminate upfront costs entirely

- Government subsidy programs like PM-KUSUM that reduce overall project costs

The fundamental shift in solar financing has transformed the value proposition. Instead of asking “Can I afford solar?”, customers now ask “Which financing option maximizes my solar ROI?” This guide will help you answer that question with confidence.

What Are the Main Types of Solar Financing Options Available in 2026?

Understanding the landscape of solar financing options is essential for making an informed decision. Each financing method comes with distinct advantages, eligibility requirements, and long-term implications. Let’s explore the primary options available to customers in Gujarat and across India in 2026.

Solar Loans: Own Your System, Finance the Cost

Solar loans are the most popular financing option for both residential and commercial customers. With a solar loan, you own the solar energy system from installation day, which means you benefit from all incentives, tax benefits, and the full value of electricity savings. Banks, non-banking financial companies (NBFCs), and specialized green energy lenders offer solar loans with terms typically ranging from 5 to 20 years.

Key characteristics of solar loans:

- Interest rates typically range from 8.5% to 14% depending on your credit profile

- Loan amounts can cover up to 100% of the project cost

- You own the system and all associated benefits

- Secured loans (against property) offer lower interest rates than unsecured loans

- Monthly payments often equal or are less than your previous electricity bills

Solar Leases: Use Solar Without Ownership

A solar lease allows you to have a solar system installed on your property without purchasing it. You pay a fixed monthly lease payment to the solar company that owns and maintains the system. This option is particularly attractive for customers who want predictable costs without ownership responsibilities.

Solar lease characteristics:

- No upfront costs in most cases

- Fixed monthly payments for the lease term (typically 15-25 years)

- The solar company owns, maintains, and monitors the system

- Immediate electricity savings from day one

- No responsibility for system performance or maintenance

Power Purchase Agreements (PPAs): Pay Only for Solar Electricity

Under a PPA, a solar company installs and owns the solar system on your property, and you agree to purchase the electricity it generates at a predetermined rate. This rate is typically lower than grid electricity rates, ensuring immediate savings. PPAs are especially popular for commercial and industrial solar Gujarat installations.

PPA characteristics:

- Zero upfront investment required

- You pay only for the electricity generated (per kWh rate)

- Rates are usually 10-20% lower than grid electricity

- The solar provider handles all maintenance and performance risks

- Contract terms typically span 20-25 years

Zero-Down Payment Financing

Zero-down payment schemes have gained tremendous popularity in 2026, combining elements of loans and leases to eliminate upfront costs entirely. These programs allow customers to start saving on electricity immediately while financing the system through monthly payments that are often lower than previous utility bills.

Government Subsidies and Incentive Programs

The Indian government offers substantial subsidies for residential rooftop solar installations and agricultural solar projects. The PM-KUSUM scheme and state-level programs in Gujarat provide capital subsidies that can reduce your project cost by 30-40% for eligible installations. These subsidies can be combined with other financing options to further reduce your financial burden.

When working with experienced solar EPC Gujarat providers like Heaven Green Energy, you receive guidance on accessing these subsidies and integrating them into your overall financing strategy.

Solar Loans: Frequently Asked Questions

Solar loans remain the most straightforward path to solar ownership, but many customers have questions about how they work, eligibility requirements, and long-term implications. Here are the most common questions we receive about solar financing through loans.

What is a solar loan and how does it work?

A solar loan is a specialized financing product designed specifically for purchasing and installing solar energy systems. It works similarly to a home improvement loan or auto loan—you borrow money to purchase the solar system, and you repay the loan with interest over a predetermined period. The key advantage is that your monthly loan payment is often offset by the electricity savings you generate from the solar system.

For example, if your current electricity bill is ₹8,000 per month and your solar loan payment is ₹6,500 per month while your new electricity bill drops to ₹1,000, you’re immediately cash-flow positive by ₹500 monthly. After the loan is paid off, you enjoy free electricity for the remaining lifespan of your system (typically 25+ years).

What are the typical interest rates for solar loans in India?

As of 2026, solar loan interest rates in India vary based on several factors including your credit score, loan amount, loan tenure, and whether the loan is secured or unsecured. Here’s what you can typically expect:

- Secured solar loans: 8.5% to 11.5% per annum

- Unsecured solar loans: 11% to 14% per annum

- Government-backed green energy loans: 7.5% to 10% per annum

- NBFC solar loans: 10% to 15% per annum

Many banks and financial institutions offer preferential rates for solar installations because they’re considered environmentally beneficial investments with strong solar ROI potential. Your actual rate will depend on your creditworthiness and the lender’s current offerings.

What is the difference between secured and unsecured solar loans?

The distinction between secured and unsecured solar loans significantly impacts your interest rate and loan terms:

Secured Solar Loans: These loans require collateral, typically your property or the solar system itself. Because the lender has security against the loan, they offer lower interest rates (usually 2-3% lower than unsecured loans). Secured loans are ideal for larger commercial or industrial solar Gujarat installations where the project cost is substantial. The approval process takes longer due to property valuation requirements.

Unsecured Solar Loans: These loans don’t require collateral, making them faster to process and more accessible for residential customers. However, they come with higher interest rates to compensate for the lender’s increased risk. Unsecured loans are perfect for smaller residential rooftop solar Gujarat projects where quick approval and minimal documentation are priorities.

What documents are required for solar loan approval?

Documentation requirements vary by lender, but most solar loan applications require:

- Identity proof (Aadhaar card, PAN card, passport, or driver’s license)

- Address proof (utility bills, property documents, or rental agreement)

- Income proof (salary slips, bank statements, or ITR for last 2-3 years)

- Property ownership documents (for secured loans)

- Solar installation quotation from a registered solar EPC company

- Photographs (passport-size)

- Bank account statements for the last 6 months

When you work with established solar companies Gujarat like Heaven Green Energy, we often assist with the documentation process and have partnerships with lenders that can streamline approval.

How long are typical solar loan terms?

Solar loan tenures in India typically range from 5 to 20 years, with the most common terms being:

- 5-7 years: Higher monthly payments but lower total interest paid

- 10-12 years: Balanced approach with moderate monthly payments

- 15-20 years: Lower monthly payments but higher total interest cost

The optimal loan tenure depends on your cash flow situation and solar payback goals. Many customers choose a tenure that ensures their monthly loan payment plus reduced electricity bill is less than their previous electricity expense, creating immediate positive cash flow.

Can I get tax benefits with a solar loan?

Yes, solar loans can provide tax benefits, though the specifics depend on whether you’re a residential or commercial customer. For businesses, the depreciation benefits on solar assets can be substantial—up to 40% accelerated depreciation in the first year under current tax regulations. Commercial and industrial customers can also claim interest paid on solar loans as a business expense.

For residential customers, while direct tax deductions on solar loans are limited, you benefit from the capital solar subsidy programs that reduce your overall project cost. Additionally, the electricity savings are tax-free income in the form of reduced expenses.

Solar Leases and PPAs: What You Need to Know

While solar loans provide ownership, leases and Power Purchase Agreements (PPAs) offer alternative paths to solar adoption without the responsibilities of ownership. These options have become increasingly popular for commercial customers and homeowners who prefer predictable costs without maintenance concerns.

What is a solar lease and how does it differ from buying?

A solar lease is essentially a rental agreement for a solar energy system. The solar company installs, owns, and maintains the system on your property, and you pay a fixed monthly lease payment for the right to use the electricity it generates. This differs fundamentally from buying (whether through cash or loan) in several ways:

Ownership: With a lease, you never own the system. The solar company retains ownership throughout the lease term and typically removes the system at the end of the contract (though you may have a purchase option).

Maintenance responsibility: The leasing company handles all maintenance, repairs, and system monitoring. If performance drops or equipment fails, it’s their responsibility to fix it at no cost to you.

Incentives and subsidies: The leasing company claims all government subsidies, tax benefits, and renewable energy certificates. You benefit indirectly through lower lease payments, but you don’t receive these incentives directly.

Long-term value: After a loan is paid off, you own the system and enjoy free electricity. With a lease, you continue making payments throughout the term, and the system is removed unless you purchase it.

What is a Power Purchase Agreement (PPA)?

A PPA is a financial arrangement where a solar developer installs, owns, and operates a solar system on your property, and you agree to purchase the electricity it generates at a predetermined rate per kilowatt-hour (kWh). This model is particularly popular for commercial and industrial solar Gujarat installations.

Under a typical PPA structure:

- The solar company invests all capital for system design, equipment, and installation

- You sign a long-term agreement (usually 20-25 years) to purchase the solar electricity

- The PPA rate is fixed or escalates at a predetermined rate (typically 2-3% annually)

- You pay only for actual electricity generated, measured by meters

- The solar company handles all operations, maintenance, and performance risks

PPAs are especially attractive for businesses with high electricity consumption but limited capital for upfront investment. The immediate savings (typically 10-20% below grid rates) improve cash flow without affecting balance sheets.

Who owns the solar system in a lease or PPA?

In both lease and PPA arrangements, the solar company retains full ownership of the system throughout the contract term. This ownership structure has important implications:

The solar company is responsible for system performance, maintenance, insurance, and monitoring. They bear the risk if the system underperforms or requires repairs. This arrangement is managed by experienced solar EPC services providers who have the expertise and resources to maintain optimal system performance.

At the end of the contract term, you typically have three options: extend the agreement at a reduced rate, purchase the system at fair market value, or have the system removed at no cost to you.

What are the advantages and disadvantages of leasing?

Advantages of solar leasing:

- Zero or minimal upfront costs make solar accessible immediately

- Predictable monthly payments simplify budgeting

- No maintenance responsibilities or unexpected repair costs

- Professional monitoring ensures optimal system performance

- Immediate electricity savings from day one

- No impact on credit utilization (unlike loans)

Disadvantages of solar leasing:

- You don’t own the system, so you miss out on ownership benefits

- Total payments over the lease term may exceed the system’s purchase price

- You don’t receive government subsidies or tax benefits directly

- Selling your property can be complicated with an active lease

- Less flexibility to upgrade or modify the system

- Long-term contracts (15-25 years) create extended obligations

How do maintenance and warranties work with leases?

One of the most attractive aspects of solar leases and PPAs is comprehensive maintenance coverage. The solar company is contractually obligated to maintain system performance, which includes:

Routine maintenance: Regular cleaning of solar modules, inspection of electrical connections, and performance monitoring are all handled by the leasing company. This is particularly valuable in Gujarat’s climate where dust accumulation can impact efficiency.

Repairs and replacements: If components fail—whether it’s a solar inverter, module, or other equipment—the leasing company replaces them at no cost to you. This eliminates the risk of unexpected expenses.

Performance guarantees: Most lease agreements include performance guarantees, typically 85-90% of projected output. If the system underperforms, the leasing company must remedy the situation or compensate you.

Warranty management: The leasing company manages all solar warranty claims with manufacturers, handling the administrative burden and ensuring equipment issues are resolved promptly.

Can businesses benefit from solar PPAs?

Absolutely. PPAs are particularly well-suited for commercial and industrial businesses for several compelling reasons:

Capital preservation: Businesses can adopt solar without diverting capital from core operations. The solar company makes the investment, and you benefit from reduced electricity costs immediately.

Off-balance-sheet financing: Since you don’t own the asset, it doesn’t appear on your balance sheet, preserving debt capacity for other business needs.

Predictable energy costs: With fixed or slowly escalating PPA rates, businesses can forecast energy expenses accurately, unlike volatile grid electricity prices.

Sustainability goals: Companies can meet corporate sustainability targets and reduce carbon footprints without capital expenditure.

Scalability: PPAs work well for large installations where the capital requirement would be prohibitive. Many industrial solar Gujarat projects exceeding 500 kW are structured as PPAs.

At Heaven Green Energy, we’ve structured numerous PPA arrangements for commercial clients across Gujarat, helping them achieve energy cost savings of 15-25% while advancing their sustainability objectives.

Zero-Down Payment Solar Financing: Is It Right for You?

Zero-down payment solar financing has revolutionized solar accessibility in 2026, eliminating the primary barrier that prevented many homeowners and businesses from adopting solar energy. But how do these programs work, and are they truly as beneficial as they sound?

What does zero-down payment solar financing mean?

Zero-down payment financing means you can have a complete solar energy system installed on your property without paying anything upfront. The entire cost of equipment, installation, permits, and commissioning is financed, and you begin making monthly payments only after the system is operational and generating electricity.

These programs typically combine elements of traditional solar loans with innovative financing structures. The monthly payment is calculated to be equal to or less than your current electricity bill, ensuring you’re cash-flow positive or neutral from day one.

How do zero-down schemes work in practice?

Here’s a typical zero-down payment solar financing structure:

Step 1: System design and quotation: A qualified solar EPC Gujarat provider like Heaven Green Energy assesses your property, designs an optimal system, and provides a detailed quotation including all costs.

Step 2: Financing approval: You apply for financing through the solar company’s lending partners. The approval process considers your credit score, income, and property ownership but doesn’t require upfront payment.

Step 3: Installation: Once approved, the solar company proceeds with installation. All costs are covered by the financing arrangement.

Step 4: Commissioning and connection: After installation, the system is commissioned, connected to the grid (for net metering), and begins generating electricity.

Step 5: Monthly payments begin: You start making monthly payments to the lender, typically structured so that your payment plus reduced electricity bill equals or is less than your previous electricity expense.

What are the eligibility criteria?

Zero-down payment programs have specific eligibility requirements to manage lender risk:

- Credit score: Most programs require a minimum credit score of 650-700. Higher scores may qualify for better interest rates.

- Property ownership: You must own the property where the solar system will be installed, or have landlord permission with a long-term lease.

- Income verification: Stable income documentation is required to demonstrate repayment capacity.

- Property condition: The roof or installation area must be structurally sound and suitable for solar installation.

- Electricity consumption: Minimum monthly electricity bills (typically ₹3,000-5,000) ensure the financing makes economic sense.

- Location: The property must be in the lender’s service area with adequate solar irradiation.

Are there hidden costs or higher interest rates?

This is a critical question that deserves an honest answer. Zero-down payment programs are not “free money”—they’re financing products with specific terms and costs:

Interest rates: Zero-down programs typically carry interest rates 1-2% higher than traditional solar loans with down payments. This compensates lenders for the increased risk of 100% financing. Rates usually range from 10-14% depending on your credit profile.

Longer loan terms: To keep monthly payments low, zero-down programs often extend loan terms to 15-20 years, which means you’ll pay more total interest over the life of the loan.

Origination fees: Some programs charge processing or origination fees (typically 1-3% of loan amount), though these are often rolled into the financed amount rather than paid upfront.

Equipment specifications: To keep costs manageable, some zero-down programs may specify particular solar brands Gujarat or equipment tiers. Ensure you’re getting quality components from reputable manufacturers.

The key is transparency. Reputable solar companies Gujarat will provide complete disclosure of all costs, interest rates, and terms. At Heaven Green Energy, we believe in full transparency, ensuring customers understand exactly what they’re committing to.

Comparison with traditional financing options

How does zero-down financing compare to other options? Here’s a practical comparison:

Zero-down vs. 20% down payment loan: A traditional loan with 20% down typically offers interest rates 1.5-2% lower and shorter loan terms. Over 15 years, this could save ₹1-2 lakhs in interest on a ₹5 lakh system. However, you need ₹1 lakh upfront, which many customers don’t have readily available.

Zero-down vs. solar lease: Zero-down loans provide ownership, meaning you benefit from subsidies, tax benefits, and full system value. Leases offer similar zero-upfront structure but without ownership benefits. After 20 years, the loan results in system ownership while the lease ends with no asset.

Zero-down vs. cash purchase: Cash purchase offers the best solar ROI with no interest costs and fastest solar payback period (typically 4-6 years). However, it requires significant capital. Zero-down preserves your capital for other uses while still providing solar benefits.

Best scenarios for zero-down financing

Zero-down payment solar financing is ideal when:

- You have high monthly electricity bills (₹5,000+) but limited savings for upfront investment

- You want to preserve capital for other priorities while still adopting solar

- Your credit score is good (700+) but you lack liquid assets for a down payment

- You plan to stay in the property long-term (10+ years) to realize full benefits

- Immediate cash flow improvement is more important than minimizing total interest paid

- You want system ownership and associated benefits without upfront costs

Government Subsidies and Incentives for Solar Financing in Gujarat

Government support has been instrumental in making solar energy affordable across India. Understanding available subsidies and how to access them can significantly reduce your overall solar panel cost and improve your project economics. Gujarat, as a leading solar state, offers multiple incentive programs that can be combined with financing options.

Overview of PM-KUSUM scheme and eligibility

The Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan (PM-KUSUM scheme) is one of India’s most ambitious solar programs, targeting farmers and agricultural applications. The scheme has three components:

Component A: Installation of ground-mounted solar power plants (500 kW to 2 MW) on barren or fallow land. Farmers can generate income by selling electricity to distribution companies.

Component B: Installation of standalone solar-powered agriculture pumps for irrigation. The government provides 60% subsidy (30% from central government, 30% from state government), with farmers paying only 10% upfront and the remaining 30% available through financing.

Component C: Solarization of existing grid-connected agriculture pumps. Similar subsidy structure as Component B.

Eligibility for PM-KUSUM:

- Individual farmers with agricultural land

- Farmer Producer Organizations (FPOs)

- Cooperatives and Panchayats

- Water User Associations

The scheme is particularly relevant for agricultural customers in Gujarat, where irrigation costs represent a significant operational expense. Heaven Green Energy has extensive experience implementing PM-KUSUM scheme projects across Gujarat, handling the application process and subsidy documentation.

Rooftop solar subsidy programs in Gujarat

The Ministry of New and Renewable Energy (MNRE) provides capital subsidies for residential rooftop solar Gujarat installations under the Grid-Connected Rooftop Solar Programme Phase-II. As of 2026, the subsidy structure is:

- Systems up to 3 kW: 40% of benchmark cost (approximately ₹18,000 per kW)

- Systems above 3 kW and up to 10 kW: 40% for first 3 kW + 20% for additional capacity

- Example: For a 5 kW system, subsidy = (3 kW × ₹18,000) + (2 kW × ₹9,000) = ₹72,000

This subsidy is available only for residential consumers and is processed through electricity distribution companies (DISCOMs). The subsidy amount is typically adjusted in the final invoice, reducing your upfront or financed amount.

Important considerations:

- Subsidies are available only for systems installed by MNRE-empaneled vendors

- Equipment must meet specified quality standards and be from approved manufacturers

- Net metering connection is mandatory for subsidy eligibility

- The subsidy is processed after installation and inspection by DISCOM officials

How subsidies reduce overall solar panel cost

Government subsidies can dramatically improve the economics of your solar investment. Let’s look at a practical example for a residential rooftop solar Gujarat installation:

Scenario: 5 kW residential solar system in Surat, Gujarat

- System cost without subsidy: ₹3,00,000 (₹60,000 per kW)

- Government subsidy (40% for 3 kW + 20% for 2 kW): ₹72,000

- Net cost after subsidy: ₹2,28,000

- If financed with zero-down at 11% for 15 years: Monthly payment ≈ ₹2,600

- Previous electricity bill: ₹5,500/month

- New electricity bill with solar: ₹800/month

- Net monthly savings: ₹5,500 – ₹2,600 – ₹800 = ₹2,100

Without the subsidy, the monthly loan payment would be approximately ₹3,400, reducing monthly savings to ₹1,300. The subsidy effectively improves your cash flow by ₹800 per month and reduces the solar payback period by 2-3 years.

DREBP scheme benefits

The Decentralized Renewable Energy Based Power (DREBP) scheme focuses on providing renewable energy access to remote and rural areas. While primarily targeting off-grid applications, the scheme offers benefits for certain grid-connected projects as well, particularly for community-based installations.

Under DREBP, eligible projects can receive:

- Capital subsidies for community solar installations

- Support for solar mini-grids in underserved areas

- Technical assistance for project implementation

- Preferential financing terms through designated financial institutions

Heaven Green Energy has successfully implemented several DREBP projects in rural Gujarat, bringing solar energy to communities that previously lacked reliable electricity access.

How to apply for government solar subsidies

Applying for solar subsidies requires following specific procedures and working with approved vendors. Here’s the step-by-step process:

Step 1: Choose an empaneled solar installer

Only installations by MNRE-empaneled vendors qualify for subsidies. Heaven Green Energy is an empaneled vendor with extensive experience processing subsidy applications across Gujarat.

Step 2: Register on the national portal

For rooftop solar subsidies, register on the National Portal for Rooftop Solar (solarrooftop.gov.in) and submit your application with property and electricity connection details.

Step 3: Obtain feasibility approval

Your local DISCOM will conduct a feasibility study to ensure your property is suitable for solar installation and net metering.

Step 4: System installation

Once approved, the solar company proceeds with installation using approved equipment and following technical specifications.

Step 5: Inspection and commissioning

DISCOM officials inspect the installation to verify compliance with standards. After approval, the system is commissioned and connected for net metering.

Step 6: Subsidy disbursement

The subsidy amount is either adjusted in your final invoice or disbursed to your bank account after successful commissioning. Processing typically takes 30-90 days.

Combining subsidies with financing options

The most powerful approach to solar financing combines government subsidies with appropriate financing mechanisms. Here’s how to maximize benefits:

Subsidy + Zero-down financing: The subsidy reduces the financed amount, lowering your monthly payments. For a ₹3 lakh system with ₹72,000 subsidy, you finance only ₹2.28 lakhs, reducing monthly payments by approximately 25%.

Subsidy + Traditional loan: Use the subsidy to reduce your down payment requirement. If a lender requires 20% down (₹60,000 on a ₹3 lakh system), the ₹72,000 subsidy more than covers this, potentially leaving you with excess funds.

Subsidy + Partial cash payment: If you have some savings but not enough for full cash purchase, use your savings for partial payment and finance the balance after subsidy adjustment. This minimizes interest costs while preserving some capital.

When you work with experienced solar EPC services providers like Heaven Green Energy, we help structure your financing to maximize subsidy benefits and minimize overall costs. Our team handles all subsidy documentation and DISCOM coordination, ensuring a smooth process from application to disbursement.

How to Choose the Best Solar Financing Option for Your Needs

With multiple solar financing options available, choosing the right one requires careful evaluation of your financial situation, energy needs, and long-term goals. This section provides a framework for making an informed decision that maximizes your solar ROI while aligning with your circumstances.

Assessing your financial situation and credit score

Your financial profile is the foundation of your financing decision. Start by honestly evaluating:

Available capital: How much can you comfortably invest upfront without compromising emergency funds or other financial obligations? If you have substantial savings, cash purchase or a large down payment loan offers the best long-term value. If capital is limited, zero-down or lease options become more attractive.

Credit score: Your credit score directly impacts available financing options and interest rates. Check your CIBIL score before exploring financing:

- 750+: Excellent – qualify for best rates and all financing options

- 700-749: Good – qualify for most options with competitive rates

- 650-699: Fair – qualify for financing but with higher interest rates

- Below 650: Limited options – may need to consider lease/PPA or work on improving credit first

Monthly cash flow: Calculate your comfortable monthly payment capacity. Your solar payment should fit within your budget while still providing net savings compared to current electricity costs.

Tax situation: For businesses, consider your tax liability and ability to utilize depreciation benefits. If you have significant tax liability, ownership (through loan or cash) provides valuable tax advantages. If tax benefits are limited, a PPA might be more suitable.

Calculating solar ROI with different financing methods

Understanding the return on investment for each financing option helps you make data-driven decisions. Here’s how to calculate and compare solar ROI:

Cash purchase ROI calculation:

- Total investment: ₹3,00,000 (5 kW system)

- Annual electricity savings: ₹60,000

- Annual maintenance cost: ₹5,000

- Net annual benefit: ₹55,000

- Simple payback period: 5.45 years

- 25-year ROI: 358% (₹13.75 lakhs savings on ₹3 lakh investment)

Solar loan ROI calculation (11% interest, 15 years):

- Total investment: ₹3,00,000

- Total interest paid: ₹2,10,000

- Total cost: ₹5,10,000

- 25-year electricity savings: ₹15,00,000

- Net benefit: ₹9,90,000

- ROI: 194%

Solar lease ROI calculation (₹2,500/month for 20 years):

- Total lease payments: ₹6,00,000

- Electricity savings during lease: ₹12,00,000

- Net benefit during lease: ₹6,00,000

- No ownership after lease ends

- 20-year ROI: 100% (but no asset ownership)

These calculations demonstrate that while cash purchase offers the highest ROI, financed options still provide substantial returns while preserving capital and providing immediate benefits.

Residential vs commercial/industrial considerations

The optimal financing approach differs significantly between residential and commercial/industrial applications:

Residential considerations:

- Smaller system sizes (1-10 kW) make cash purchase more feasible

- Government subsidies available only for residential installations

- Simpler decision-making process with fewer stakeholders

- Personal credit score and income are primary factors

- Emotional factors (environmental values, energy independence) play larger role

- Zero-down and traditional loans are most popular options

Commercial/industrial considerations:

- Larger system sizes (50 kW to several MW) require substantial capital

- Tax benefits (depreciation) are significant and should be factored into decisions

- Multiple stakeholders and approval processes

- Business credit and financial statements determine eligibility

- ROI and payback period are primary decision factors

- PPAs and secured loans are common for large industrial solar Gujarat projects

- Off-balance-sheet financing (PPA) may be preferred to preserve debt capacity

For commercial clients, Heaven Green Energy provides detailed financial modeling that incorporates tax benefits, depreciation schedules, and electricity cost escalation to present a complete picture of each financing option’s impact on your business.

Understanding solar payback periods with financing

The solar payback period—the time required to recover your investment through electricity savings—varies significantly based on your financing choice:

Cash purchase: 4-6 years in Gujarat’s favorable solar conditions. After payback, you enjoy 19-21 years of essentially free electricity (minus minimal maintenance costs).

Solar loan: The payback period extends to the loan tenure (typically 10-15 years) since you’re paying both principal and interest. However, you’re often cash-flow positive from day one, meaning your monthly savings exceed your loan payment.

Zero-down financing: Similar to traditional loans but with slightly longer payback due to higher interest rates. The advantage is immediate adoption without capital requirement.

Lease/PPA: These don’t have a traditional payback period since you never own the system. Instead, evaluate cumulative savings over the contract term. You save money monthly but never achieve “free electricity” since payments continue throughout the term.

Questions to ask your solar EPC provider

When evaluating financing options with solar companies Gujarat, ask these critical questions:

- What is the total cost of the system including all equipment, installation, and commissioning?

- Which solar brands and equipment models will be used? Verify they’re from reputable manufacturers with strong solar warranty terms.

- What financing options do you offer, and what are the complete terms? Get details on interest rates, tenure, processing fees, and any hidden costs.

- Are you MNRE-empaneled for subsidy processing? This is essential for accessing government subsidies.

- What is included in your maintenance package? Understand what’s covered and for how long.

- What performance guarantees do you provide? Reputable providers guarantee minimum system performance.

- Can you provide references from similar projects? Speak with previous customers about their experience.

- How do you handle warranty claims and system issues? Understand the support process.

- What happens if I want to sell my property? Understand implications for each financing type.

Red flags to watch out for in financing offers

Protect yourself by recognizing warning signs of problematic financing arrangements:

- Pressure tactics: Legitimate providers give you time to evaluate options. High-pressure sales suggesting “limited time offers” are red flags.

- Unclear pricing: If the provider can’t clearly explain all costs, interest rates, and terms, walk away.

- Unknown equipment brands: Insist on recognized solar brands Gujarat with established track records and warranty support.

- No written contracts: Everything should be documented in detailed written agreements.

- Unrealistic performance claims: Be skeptical of providers promising savings that seem too good to be true.

- No license or credentials: Verify the provider is properly licensed and has relevant certifications.

- Upfront payment demands: While deposits are normal, be cautious of providers demanding full payment before installation.

- Lack of local presence: Choose providers with established local operations and service capabilities.

Solar Financing Eligibility and Application Process

Understanding eligibility requirements and the application process for solar financing helps you prepare properly and avoid delays. While specific requirements vary by lender and financing type, this section covers the common elements you’ll encounter.

Who qualifies for solar financing?

Solar financing is available to a broad range of customers, but lenders have specific criteria to manage risk:

Residential customers qualify if they:

- Own the property where solar will be installed (or have long-term lease with landlord permission)

- Have a minimum credit score (typically 650-700, varies by lender)

- Demonstrate stable income through employment or business

- Have an active electricity connection with minimum consumption levels

- Are Indian citizens or residents with valid identification

- Have no major outstanding defaults or legal issues

Commercial/industrial customers qualify if they:

- Are registered businesses with minimum operational history (typically 2-3 years)

- Own or have long-term lease on the property

- Demonstrate business profitability through financial statements

- Have adequate electricity consumption to justify the investment

- Provide business registration documents and tax compliance proof

Credit score requirements

Your credit score is one of the most important factors in financing approval and interest rate determination. Here’s how different score ranges impact your options:

750+ (Excellent): You’ll qualify for the best interest rates (8.5-10% for secured loans) and most favorable terms. Lenders view you as low-risk, and you may negotiate better conditions.

700-749 (Good): You’ll qualify for competitive rates (9-11%) and have access to most financing products. This is the minimum score many premium lenders require.

650-699 (Fair): You’ll qualify for financing but with higher interest rates (11-13%). Some lenders may require larger down payments or additional documentation.

Below 650 (Poor): Traditional financing may be difficult. Consider lease/PPA options that don’t rely on personal credit, or work on improving your credit score before applying. Some specialized lenders serve this segment but with significantly higher rates (14-16%).

If your credit score is lower than desired, consider these steps before applying:

- Pay down existing debts to improve credit utilization ratio

- Ensure all current EMIs are paid on time for 6+ months

- Correct any errors in your credit report

- Avoid applying for multiple loans simultaneously

Income and property ownership criteria

Income requirements: Lenders want assurance you can comfortably afford monthly payments. General guidelines include:

- Salaried individuals: Minimum monthly income of ₹25,000-30,000 for residential solar loans

- Self-employed: Minimum annual income of ₹3-4 lakhs with proof through ITR

- Debt-to-income ratio: Your total monthly debt obligations (including the proposed solar loan) should not exceed 50-60% of monthly income

Property ownership: Most financing options require you to own the property where solar will be installed. This provides security for the lender and ensures you’ll benefit from the long-term investment. Requirements include:

- Clear property title in your name

- Property documents (sale deed, property tax receipts)

- For secured loans, property valuation may be required

- For leased properties, landlord permission and minimum remaining lease term (typically 10+ years)

Step-by-step application process

Here’s what to expect when applying for solar financing in Gujarat:

Step 1: Initial consultation (1-2 days)

Contact a qualified solar EPC Gujarat provider like Heaven Green Energy. We assess your property, review your electricity bills, and discuss your energy needs and financial situation. This consultation is typically free and helps determine the optimal system size and financing approach.

Step 2: System design and quotation (2-3 days)

Based on the site assessment, we design a customized solar system and provide a detailed quotation including equipment specifications, installation scope, and total cost. This quotation is required for financing applications.

Step 3: Financing application (1-2 days)

You submit a financing application with required documents. Many solar companies have partnerships with lenders and can facilitate this process. Applications can often be submitted online or through the solar company.

Step 4: Document verification (3-5 days)

The lender reviews your application and documents. They may request additional information or clarification. Respond promptly to avoid delays.

Step 5: Credit assessment and approval (5-10 days)

The lender conducts credit checks, verifies income, and assesses risk. For secured loans, property valuation may occur during this phase. You’ll receive an approval decision with specific terms (loan amount, interest rate, tenure).

Step 6: Agreement signing (1-2 days)

Once approved, you review and sign loan agreements. Read all terms carefully and ask questions about anything unclear. This is also when you sign the installation contract with the solar company.

Step 7: Installation (5-15 days)

The solar company proceeds with installation. For financed projects, the lender typically disburses funds directly to the solar company in stages (advance, post-installation, post-commissioning).

Step 8: Commissioning and connection (5-10 days)

After installation, the system is tested, commissioned, and connected to the grid for net metering. DISCOM inspection and approval are required for grid connection.

Step 9: Final disbursement and EMI start (immediate)

Once the system is operational, final loan disbursement occurs, and your EMI payments begin. You also start generating solar electricity and reducing your utility bills.

Timeline from application to installation

The complete timeline from initial inquiry to operational solar system typically ranges from 4-8 weeks, broken down as:

- Consultation and quotation: 3-5 days

- Financing approval: 7-15 days

- Installation: 5-15 days (depending on system size)

- Commissioning and grid connection: 5-10 days

Factors that can extend timelines include:

- Incomplete documentation requiring multiple submissions

- Property issues requiring additional verification

- DISCOM delays in feasibility approval or net metering connection

- Monsoon season affecting installation schedules

- Complex installations requiring structural modifications

Working with solar companies in Gujarat for financing

Choosing the right solar EPC services provider is crucial for a smooth financing and installation experience. Established companies like Heaven Green Energy offer several advantages:

Lender partnerships: We have relationships with multiple banks and NBFCs, giving you access to competitive financing options and streamlined approval processes.

Documentation support: Our team assists with preparing and organizing required documents, reducing errors and delays.

Subsidy processing: We handle all government subsidy applications and DISCOM coordination, ensuring you receive entitled benefits.

Single point of contact: Rather than coordinating separately with lenders, equipment suppliers, and installers, you work with one team managing the entire process.

Quality assurance: Established providers use quality equipment from reputable solar brands Gujarat and follow proper installation standards, protecting your investment.

After-sales support: Ongoing solar maintenance Gujarat services, warranty management, and performance monitoring ensure your system operates optimally throughout its lifespan.

When you’re ready to explore solar financing options, contact Heaven Green Energy at +91 63904 05060 to discuss your specific needs and receive personalized guidance on the best financing approach for your situation.

Common Solar Financing Mistakes to Avoid

Even with the best intentions, customers sometimes make financing decisions that reduce their solar ROI or create unexpected challenges. Learning from common mistakes helps you avoid costly errors and maximize the benefits of your solar investment.

Not comparing multiple financing offers

One of the biggest mistakes is accepting the first financing offer without shopping around. Interest rates, terms, and conditions vary significantly between lenders. A difference of just 1-2% in interest rate can mean tens of thousands of rupees over a 15-year loan term.

Best practice: Obtain quotes from at least 3-4 lenders before deciding. Compare not just interest rates but also processing fees, prepayment penalties, and flexibility in terms. Reputable solar companies Gujarat like Heaven Green Energy can help you compare options from multiple lending partners.

Ignoring the total cost of financing

Many customers focus solely on monthly payment amounts without considering the total cost over the loan term. A longer tenure with lower monthly payments might seem attractive but results in significantly more interest paid.

Example: ₹3 lakh loan at 11% interest

- 10-year term: Monthly EMI ₹4,145, total interest ₹1,97,400

- 15-year term: Monthly EMI ₹3,415, total interest ₹3,14,700

- Difference: ₹1,17,300 more interest for the longer term

Best practice: Calculate and compare total interest paid for different loan tenures. Choose the shortest tenure you can comfortably afford to minimize total cost while ensuring monthly payments fit your budget.

Overlooking warranty and maintenance terms

Solar systems require minimal but important maintenance, and equipment warranties are crucial for long-term performance. Some customers focus entirely on financing terms while neglecting to verify warranty coverage and maintenance provisions.

Critical warranty elements:

- Solar module warranty: Minimum 25-year performance warranty (typically 80% output after 25 years)

- Solar inverter warranty: Minimum 5-10 years (inverters typically need replacement after 10-15 years)

- Installation warranty: Minimum 5-year workmanship warranty from the installer

- Maintenance terms: Clear understanding of what’s included and what costs extra

Best practice: Verify all warranty terms in writing before finalizing financing. Understand who handles warranty claims and what the process involves. Factor potential inverter replacement costs into your long-term financial planning.

Failing to verify solar brands and equipment quality

Not all solar equipment is created equal. Some financing offers seem attractive because they use lower-quality, cheaper equipment that may underperform or fail prematurely. This defeats the purpose of your investment.

Best practice: Insist on equipment from established, reputable manufacturers with proven track records in India. Ask specifically about:

- Solar module brand, model, and efficiency ratings

- Inverter brand, type (string vs. micro), and specifications

- Mounting structure materials and wind load ratings

- Cable and electrical component specifications

Heaven Green Energy uses only quality equipment from recognized solar brands Gujarat with established service networks, ensuring your system performs reliably for decades.

Not understanding contract terms fully

Solar financing contracts contain important terms that affect your rights and obligations. Signing without fully understanding these terms can lead to unpleasant surprises.

Critical contract elements to understand:

- Prepayment terms: Can you pay off the loan early? Are there penalties?

- Default consequences: What happens if you miss payments?

- System ownership: When do you take full ownership? (Important for leases/PPAs)

- Maintenance obligations: What are you responsible for vs. what the provider handles?

- Performance guarantees: What recourse do you have if the system underperforms?

- Transfer provisions: What happens if you sell your property?

Best practice: Read all contracts thoroughly before signing. Don’t hesitate to ask questions or request clarification on any terms you don’t understand. Consider having a lawyer review contracts for large commercial installations.

Skipping professional solar EPC services

Some customers attempt to save money by working with inexperienced installers or trying DIY approaches for certain aspects. This is a false economy that often results in poor system performance, safety issues, and problems accessing financing or subsidies.

Risks of unprofessional installation:

- Improper system design leading to underperformance

- Safety hazards from incorrect electrical work

- Inability to access government subsidies (requires empaneled vendors)

- Warranty voidance due to improper installation

- Difficulty obtaining net metering approval from DISCOMs

- No recourse if problems arise after installation

Best practice: Work with established, licensed solar EPC Gujarat providers with proven track records. Verify credentials, check references, and ensure they’re MNRE-empaneled for subsidy processing. The slightly higher cost of professional services is more than offset by proper installation, warranty protection, and peace of mind.

Making Solar Energy Affordable: Your Next Steps

Understanding solar financing options is the first step toward energy independence and significant long-term savings. Whether you’re a homeowner looking to reduce electricity bills or a business seeking to lower operational costs, the right financing approach makes solar accessible regardless of your available capital.

The key takeaways from this comprehensive guide include:

- Multiple financing options exist to suit different financial situations—from traditional loans and zero-down schemes to leases, PPAs, and government subsidies

- Ownership matters for maximizing long-term value, but non-ownership options like leases and PPAs provide immediate benefits without capital requirements

- Government subsidies can reduce your solar panel cost by 30-40% for eligible installations, significantly improving project economics

- Total cost matters more than monthly payment—evaluate the complete financial picture including interest paid over the loan term

- Quality equipment and professional installation are non-negotiable for achieving promised performance and solar ROI

- Your specific situation determines the best option—there’s no one-size-fits-all solution

Action steps for getting started with solar financing

Ready to move forward with your solar project? Follow these steps:

1. Assess your current situation: Review your electricity bills for the past year, check your credit score, and evaluate your available capital and monthly budget for solar payments.

2. Calculate your solar potential: Determine how much roof space you have available and estimate the system size that would meet your energy needs. A 1 kW system typically requires 100 square feet of shadow-free roof space and generates approximately 4-5 units of electricity daily in Gujarat.

3. Research financing options: Based on your financial situation, identify which financing approaches are most suitable. Consider both immediate cash flow impact and long-term total cost.

4. Contact qualified solar providers: Reach out to established solar installation Gujarat companies for site assessments and quotations. Ensure they’re MNRE-empaneled and have experience with your preferred financing type.

5. Compare detailed proposals: Obtain written proposals from multiple providers including system specifications, equipment details, financing terms, and total costs. Compare not just on price but on equipment quality, warranty terms, and company reputation.

6. Verify credentials and references: Check the provider’s licenses, certifications, and past project portfolio. Speak with previous customers about their experience.

7. Understand all terms before signing: Review all contracts, financing agreements, and warranty documents thoroughly. Ask questions about anything unclear.

8. Plan for long-term maintenance: Understand what maintenance your system will require and ensure you have a plan for ongoing care, whether through the provider or your own arrangements.

How Heaven Green Energy can help with financing guidance

At Heaven Green Energy Limited, we’ve been helping customers across Gujarat navigate solar financing since 2017. Our comprehensive approach includes:

Personalized financial consultation: We assess your specific situation and recommend financing options that maximize your benefits while fitting your budget and goals.

Multiple financing partnerships: Our relationships with leading banks and NBFCs give you access to competitive rates and terms from multiple lenders.

Subsidy processing expertise: As an MNRE-empaneled vendor, we handle all government subsidy applications and DISCOM coordination, ensuring you receive entitled benefits without hassle.

Quality equipment guarantee: We use only proven equipment from reputable solar brands Gujarat, backed by comprehensive warranties and our own workmanship guarantee.

Turnkey EPC services: From initial design through installation, commissioning, and ongoing maintenance, we provide complete solar EPC services ensuring your project succeeds.

Transparent pricing: We provide detailed, itemized quotations with no hidden costs, so you understand exactly what you’re paying for.

After-sales support: Our commitment doesn’t end at installation. We provide ongoing solar maintenance Gujarat services, performance monitoring, and warranty management throughout your system’s lifetime.

With over 10,000 installations across Gujarat and recognition as one of the top 3 EPC companies in the state, Heaven Green Energy has the experience and expertise to guide you through every aspect of your solar journey—from financing to final commissioning and beyond.

Take the first step toward energy independence

The transition to solar energy is one of the smartest financial and environmental decisions you can make in 2026. With flexible solar financing options, government support, and experienced partners like Heaven Green Energy, there’s never been a better time to go solar.

Don’t let upfront costs prevent you from enjoying the benefits of clean, renewable energy and significant electricity savings. Whether you’re interested in residential rooftop solar Gujarat, commercial installations, or large-scale industrial solar Gujarat projects, we have the expertise and financing solutions to make your solar vision a reality.

Ready to explore your solar financing options? Contact Heaven Green Energy today at +91 63904 05060 to schedule a free consultation and site assessment. Our team will evaluate your property, discuss your energy needs and financial situation, and recommend the optimal solar solution with financing that works for you.

The sun is shining, and your solar future is waiting. Let’s make it happen together.